First-Time Home Buyers

Why Start Now?

Getting yourself financially positioned to get a mortgage and purchase a home often takes time and effort. Many things need to line up including your employment/income, credit history, and down payment to name a few. This comes easy for some, and for others there are specific things you would appreciate knowing well in advance of applying for a mortgage so that necessary corrective action is possible. It's comforting to know you are headed in the right direction, and that's the goal of our team - to help you buy your first home.

![How to Buy a House [Read Guide]](https://no-cache.hubspot.com/cta/default/115190/430ef4af-ee71-4ea9-8c5c-2fede32e4fcd.png)

Every month that you wait, you flush your hard earned rent money down the toilet. Renting is wasting money because you don't control an appreciating asset. However, if you put those rent same dollars into a house payment instead of rent, you create equity ... value that you own, that later can send your kids to college, finance the start-up of your own business, or pay for your retirement. Be your own landlord and build up future financial security. We'll even show you easy strategies to speed up the payoff of your home without making extra payments. There's no reason to wait. We can help put you in a home right now or very, very soon. Switching from renting to home ownership can help you go from dependent on your landlord to financial security. You can use home ownership as the foundation of a complete change in your overall finances!

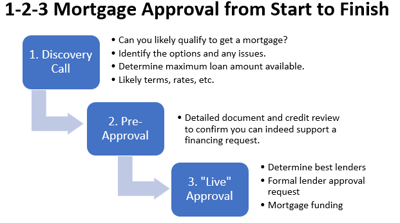

Before anything else, you need to know can you even qualify for a mortgage, then how much you can afford. The availability of mortgage financing is obviously important to your purchase plans, and each mortgage lender has their own lending guidelines, or Rule Book. Besides the lenders' Rule Book, there is another set of rules whenever you have less than 20% down payment, as your lender will need Mortgage Default Insurance.

So when figuring out how much home you can afford, your mortgage professional must refer to the Rule Books that apply to your situation. The amount you can afford also depends on five variables:

Interest rates change with the market, so you'll want to find out what the current rates are. Interest rates are lower for borrowers with good credentials, which serves to increase the mortgage payment you can afford to pay. However, rates are not necessarily lower for borrowers with less-than-stellar credentials as they represent more risk to the lender. Also understand that there is a lot more to a mortgage than rate.

Required down payments are lower for borrowers with good credentials, which means you can qualify sooner. For borrowers with less-than-stellar credentials, larger down payments are required as they represent more risk to the lender. More About Down Payment.

The income used to qualify for a mortgage may be lower than the would-be purchasers believe they have, as certain forms of income are ineligible. The amount of debt you have is also important. More About Income & Debt.

The more monthly payments a person has (credit cards, vehicle loans, lines of credit, etc.) the less of their income they have available for the mortgage payment, which serves to decrease the how much house they can afford to buy. More About Debts

When people lend you money, do you pay them back on time and as agreed? Every time you access credit/borrow money, whether credit card, cell phone, vehicle loan, student loan, etc., your repayment history and reliability is tracked by credit reporting agencies such as Equifax and TransUnion. Your credit score is a numeric value representing the likelihood you will pay back your debts reliably. The higher the better.

![Can You Get a Mortgage? [Read Now]](https://no-cache.hubspot.com/cta/default/115190/8d35a884-2a8a-444b-9ae9-a8d85af5b10a.png)

Once you know how much you can afford, there are a few steps you’ll have to tackle before you can get the keys to your new home. Here’s a broad overview of what you can expect.

1. Check Out the Neighbourhood

Before you begin looking at houses, narrow in on your chosen location.

2. Establish your home buying team

Having the right team in your corner can make all the difference when it comes to buying your first home. Your home buying team can bring a wealth of real estate experience and expertise that will help make the process as simple and straightforward as possible. Team members will often include your Realtor, Lender or Mortgage Broker, Home Inspector, Appraiser, Lawyer, Insurance Broker, Land Surveyour, and Mover. Often you will find that your Realtor and Mortgage Broker can provide top quality referrals to professionals they have good success with.

3. Get pre-approved for a mortgage

If you haven't already, this is where you will decide how much you can afford. When it comes to choosing a mortgage that works for you, start by asking yourself a few questions. Are you likely to get the financing you need? What will you do if interest rates go up before you’ve found your home? When it comes to getting pre-approved, be honest with yourself and your situation. Getting the home you want starts with getting a home you can afford. Your mortgage broker will help you answer these very important questions. Contact us for a free consultation.

4. Make an offer

Making an offer is where the rubber hits the road, often exciting and scary at the same time. Your offer will include your proposed purchase price and move-in (possession) date as well as certain conditions like your ability to secure financing, a satisfactory home inspection, and the inclusion of certain items you want included with your home purchase like appliances, window treatments or light fixtures. Often there is some back and forth between buyer and seller until the offer is accepted.

5. Finalize your mortgage

Your mortgage broker will work with you to help you get the mortgage that’s right for you. If you’ve been pre-approved for a mortgage, present your accepted offer to your broker who will advise you of any other requirements to secure the mortgage.

6. Close the deal

As the closing day approaches, it’s not unusual to feel both excited and anxious. Keep in mind your Realtor, mortgage broker and lawyer will do most of the work for you to ensure that everything goes smoothly at closing.

Obviously there are more details and a lot more to it.

Free Guide: Understand your Credit Report and Credit Score

How to Access Your Credit Report

first time home buyers tax credit

how to choose a home inspector

how to prepare for financial uncertainty

ready to be a homeowner or is renting still right for you

retail energy contracts for first time home buyers

scanning documents for your mortgage broker

my first home was in a mobile home park but i couldn't get a mortgage

how to fast track the home buying process

why a pre approval should be a first time homebuyer first step

Quantus Mortgage Solutions

5053 11 St SE

Calgary, AB T2H1M7

Canada

T: 403.238.3111