Can You get a mortgage?

Let's find out.

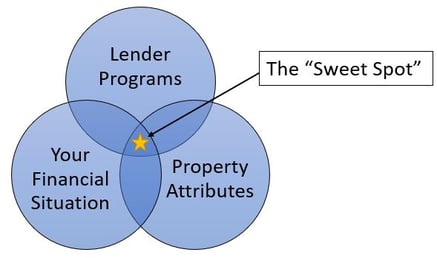

To qualify for a mortgage in Canada, the real question is, which lenders will give YOU a mortgage based on your specific financial situation *and* the type of property you seek to finance?

In a nutshell, our job as mortgage brokers is to determine which lenders will give you a mortgage, and then help you obtain favourable terms from them. It is a false assumption to think that if your bank says no, that all banks will say no, or even worse, that your bank will offer you the best terms for your unique situation. It is also a false assumption to assume that all mortgage contracts are the same. Those false assumptions can cost you a lot of time and money.

[Last updated: May 2025] To qualify for a mortgage in Canada, there are multiple interrelated variables that lenders take into consideration when determining whether the risk of lending you money is acceptable and worthwhile. Different lenders and lending products have different requirements and sometimes there are multiple or alternate solutions for your financing objectives. A systematic understanding of the mortgage qualification guidelines that lenders use to assess you as a potential borrower helps you and us set realistic goals and identify/overcome potential challenges. Here are the basics:

A quality mortgage broker can help you find and compare optimal lending solutions relative to your financial situation and property objective. They can also help you troubleshoot when things are not quite lining up. It all starts with a Discovery Call.

A mortgage is a contract between you and a lender to finance a property. To qualify for a mortgage, there are federal OSFI rules in Canada that the majority of banks and mortgage lenders must follow. This not just in Canada - since the 2007/08 financial crisis governments around the world have harmonized and imposed stricter mortgage lending conditions to better manage risk and avoid irresponsible lending behavior.

In order to assess the risk that you represent as a borrower and to decide whether they will lend you any money, lenders are required to consider 3 indicators of your financial health plus the property being mortgaged. You can use the acronym I.C.E. + P to remember the 4 requirements to qualify for a mortgage:

Think of these 4 variables like the legs on a chair that has to support your mortgage application. If one leg is a bit weak the application might still stand, but if there is more than one weak leg, the whole thing could collapse!

Finally, there are external factors, special allowances, and additional considerations that you need to be aware of that can impact a lender's willingness to lend to you.

Don't worry, you don't have to be an expert in all the lending rules, that is our job to navigate. But a little understanding is still a good idea.

We will now explore each topic in more detail. Use the anchor links below to navigate the various sections of this page and you can always click the "Table of Contents" links at the bottom right of each section to return here. There are also buttons that will open more extensive resources for each section. Feel free to use the chat box on the right hand side if you have questions at any point or reach out when you feel ready.

"You have to prove that your income is reliable and sufficient enough to pay for your new mortgage as well as your existing debts"

First, to qualify for a mortgage, you have to prove that you reliably make money. That means steady and predictable income sufficient to cover all of your payments and financial obligations, including loans, credit cards, credit lines, support payments, etc. and – of course – the new mortgage payment and property taxes.

Generally the property you can afford will be about 4 times the value of your gross (pre-tax) annual household income and potentially much less if you have a lot of other debt. This is determined by a maximum permissible ratio of monthly debts to monthly income called your debt servicing ratios.

If you have a lot of debt and payments relative to a fixed amount of income, then there might not be enough left over for the home you’d like to buy. As a rule of thumb, every $500 in monthly debt payments that you have reduces the amount of mortgage you can qualify for by $100,000 (vehicle payments are the number one culprit).

There are various permissible income sources that you can use for mortgage qualification purposes, but they need to be properly documented and show a track record that indicates that they are not likely to disappear in the foreseeable future.

Click Here to Read More About Income and Debt

“Your credit history has to demonstrate that when someone lends you money, you will likely pay them back as agreed”

Second, you need credit history on your credit report and the history needs to show – in the past 2 years at a minimum – that you have generally paid all your bills on time and that no one is chasing you to get paid.

Whether you know it or not, most organizations that lend you money or extend you credit will report your repayment patterns monthly to Equifax and TransUnion, which then show up on your credit report as a “credit score” (risk rating).

It is recommended that you have (or establish if you don't) at least 2 forms of credit that will show up on your credit report. Further, you should consistently pay your bills as agreed and on time. If you carry high balances relative to the credit limit and only make the minimum payments, that will negatively impact your credit rating hence your ability to get a mortgage.

Mortgage lenders look at your past repayment track record as a reliable predictor of your future payment habits. You don't need perfect credit, but most “A grade” lenders will generally want to see a credit score of at least 650 to 680.

The good news about credit is that it can be fixed with a little bit of discipline and time.

How to obtain a copy of your credit report

Click Here to Read More About Credit and Mortgages

“You have to have some of your own money in the deal”

Third, you’ve got to have “skin in the game,” which is the money you put into the purchase of your property. The rule book says your minimum equity / down payment needs to be 5% of the purchase price (OAC) if you are buying a house, so $20K for a $400K purchase as an example.

Additionally, you have to prove you have a further 1% set aside to cover the costs of a lawyer, property inspector, appraiser, taxes, etc., called “closing costs.”

The only way ZERO-down is an option is if you borrow the 5% separately from somewhere else, for example on a line-of-credit or a personal loan. This is only possible if you have an excellent income and credit profile.

There are various permissible sources of down payment, but like income they must be properly documented and legally obtained.

Down payment requirements for a mortgage depend on:

Click here to read More About Equity and Down Payment

“Every lender has specific rules as they relate to property type, location, attributes and intended use. What you can qualify for depends on the property in addition to your financial situation"

Each bank, trust company, mortgage investment corporation, credit union, or private lender has a list of property types, locations and uses that they will consider, and those that they won't. In some categories, such as existing single-family-homes in the city there will be intense competition and lender choice, which means better terms and conditions for you. In other categories, such as rural acreages, raw land, or new construction financing, there will be far fewer choices.

Different property types, uses and locations will influence the rate that is available to you as well down payment, credit, and income requirements. If a property's intended use is for investment purposes (rental) for example, the down payment requirement will be higher then if the property is to be owner-occupied by you, and so on.

To be considered as a target lender for you, there needs to be overlap between your financial situation and those for the property-type and/or use.

Further, lenders want to know exactly what you are buying, its physical condition, appraised value, and location. This is their "loan security" and their concern is simply: if you do not or cannot repay your mortgage and they have to take the property back (seize or foreclose on it), will they be able to sell it quickly and recover their money!

From a mortgage qualification perspective, we can either start with a given property and determine the financial requirements to obtain a loan for that property, or we can start with your financial profile as an applicant and determine what your options are in terms of properties.

Click Here for Our Property Specific Pages

Finally, in addition to ICE+P. - your Income, Credit, and Equity plus the Property - lenders make a subjective evaluation of all other conditions that might add or subtract risk in giving you a loan. For example, frequently moving around or switching employers might indicate you can't hold a job or that your industry is in trouble, hence instability. Likewise, if there is some potential income instability (economic down turn for example) do you have other assets you could sell or savings to fall back on if you run into financial hard-times or has all the money been spent? Will you or would you bring in roommates to help pay the bills? Pending divorce or unpaid income or property taxes are other examples of conditions that lenders worry about. All-in-all, lenders are about lending money while managing risk of default - that's it in a nutshell. Your job and ours is to show that you are a good candidate for a mortgage!

/carlos-alberto-gomez-iniguez-253158-unsplash-1.jpg?width=300&name=carlos-alberto-gomez-iniguez-253158-unsplash-1.jpg) If you think that you likely meet the requirements to qualify for a mortgage or think you are close and would like to discuss your situation in more detail, the first step to take would be to reach out to initiate a "discovery call" with one of us.

If you think that you likely meet the requirements to qualify for a mortgage or think you are close and would like to discuss your situation in more detail, the first step to take would be to reach out to initiate a "discovery call" with one of us.

This is a complimentary 10 to 15 minute phone conversation during where we review your property objectives as well as your ability to meet the qualifying criteria mentioned above. Be prepared to answer questions about your income, employment, tax situation, financial obligations, past credit behaviour, and your savings/assets. The goal is to determine whether your property objectives are realistic, how much you can borrow and whether you are ready to proceed with a more formal pre-approval application.

You can start by filling out our “Let’s Talk Questionnaire" and we will set up a time to call you, or you can start a conversation with us using the chat bubble that appears on most of our website pages.

After the call, we will send you an email summary of our discussion and outline your best course of action. If you are ready to proceed with an application, we will set you up with a Get Started Email, with a link to our secure mortgage application system portal, Package containing a personalized support document checklist, application form, and service agreement for you to work through.

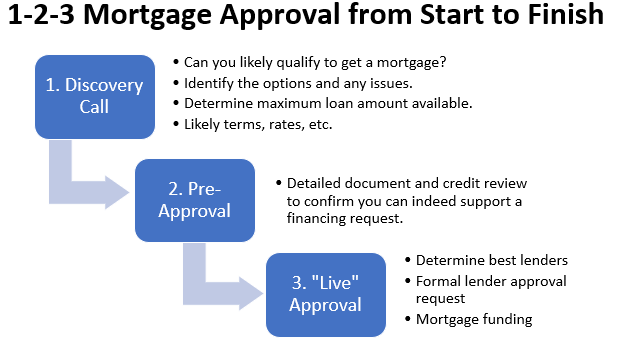

Our robust mortgage approval process is designed to provide you with reliable answers and direction from the onset such that you can make informed decisions and progress towards your property objective with confidence and clarity, and avoid false starts and wasted time.

1. Discovery Call - We discuss your financial situation (I.C.E.) and property objective (P), estimate your borrowing capacity, and identify any obstacles you may encounter. This helps you clarify your situation and provide you with an action plan to move forward, before you ever have to fill out an application.

2. Pre-Approval - We review your mortgage application and supporting documents, pull your credit report, and determine the best lenders and mortgage products for you. You will have a clear and reliable understanding of the lending options that are available to you (including a rate lock if desired) BEFORE you make any final decisions or purchase commitments. This stage should confirm the information discussed in the initial discussion and hopefully not uncover any surprises.

3. Approval - Show you the money! With the target property in mind, we submit your file to the chosen lender and work with you to meet their closing conditions. Upon the lender's final approval of your documents and the subject property, the contract is finalized and the mortgage funds.

Click Here to Read More About the Mortgage Approval Process

The exact documents requested will vary from deal to deal and from lender to lender, however we can use the I.C.E.+P framework to understand which documents will generally be required.

Income - To verify your income for a mortgage, a letter of employment, most recent paystub and tax documents such as your NOAs, T1 Generals, and T4s are the most commonly requested documents. In some cases, such as for self employed applicants, additional documentation such as business financial statements, corporate tax returns, and bank deposits can be used to verify sufficient earnings.

Credit - Before you can be approved for a mortgage, your mortgage professional will need to access your credit report and verify your credit score and outstanding liabilities. In order to do so, they will need to obtain your permission to do so with a signed and dated privacy consent form. Once your credit score has been pulled you may be asked to provide additional documentation such as monthly statements, loan agreements, or proof that an old debt was paid and closed.

Equity - To prove that you have sufficient down payment available for equity in the property, you will need to provide a 90 day transaction history for all accounts that the money has touched. Using bank statements for all accounts that the money has passed through we are required to cross reference the source of your down payment to ensure that it legally came into your possession. Any large deposits over the last 90 days will need to be explained and traced. If you have multiple accounts with sufficient money for the down payment, it is easiest to provide the account with the least or most easily explained transaction history, even if in reality you plan to use money from elsewhere. If the money is coming from the sale of an asset such as another property, you will need to provide the unconditional purchase contract and a payout statement for any associated debt. For refinances, the equity will be in your property already and an appraisal and your recent mortgage statement will be used to determine how much is available.

Property - There is a wide variety of property documents that might be asked for depending on the nature of the deal, once the property is known. For purchases, the MLS listing and purchase contract are typically required. Supplemental documents such as the land title and property tax documents may also be required. In some cases, for example a refinance, an appraisal will be needed as well and there are usually additional documentation requirements for rural properties and condos.

/tom-barrett-329280-unsplash-2.jpg?width=250&name=tom-barrett-329280-unsplash-2.jpg)

We can use the I.C.E+P. framework to understand commonly encountered obstacles and why they present a challenge for mortgage qualification. This information can be used to make a plan to get you back on track or help you think about alternate ways to achieve your objectives.

Commonly encountered challenges related to income and debt include self employment or tip income that does not show up on personal tax returns, inconsistent or non guaranteed hours or earnings, insufficient job experience, excessive debt relative to income (especially car loans), outstanding tax liabilities, and various forms of support payments. Typically it is easier to spend less than it is to earn more although there are cases where a co-signer could provide supplemental proof of income for qualifying purposes.

Credit challenges that we frequently encounter when we look at people’s credit reports are a history of late or missed payments, high credit balances relative to credit limits, too few sources of credit reporting (not enough data), to many sources of credit, and unresolved bankruptcies or consumer proposals. Bad credit can be fixed through discipline and patience, but it takes time. It is usually better to work on fixing bad credit before applying for a mortgage rather than work around it, although there are scenarios where a co-signer can support the credit of the primary applicant.

Equity constraints arise from a lack of access to financial resources. If you don’t meet the minimum 5% down payment requirements for a mortgage on your own, there are a variety of options available. If you have enough room in your debt-to-income ratios and excellent credit, you could potentially borrow the down payment from a different lender. Alternately perhaps you have an immediate family member who can gift you part or all of the down payment. You could also sell an asset such as a vehicle or other toy.

Finally, property constraints arise from a property objective that is incompatible with your financial profile as a borrower. For example, you might not meet the down payment and cash flow requirements to buy a vacant lot and build your own home. However you might be able to qualify for a loan for the same or an even better better existing property with less down. Or perhaps your original property objective is in a location that is incompatible with where you are currently employed, but there are other properties that meet your needs within a closer radius to your employer. Reassessing property objectives to focus on what you CAN achieve often uncovers unconsidered options.

The point of all of this is that mortgage finance is complicated and sometimes there are solutions for your situation that are not immediately apparent. A qualified mortgage broker with a systematic approach to understanding your objectives and challenges can help you navigate the complexities of real estate finance to arrive at a solution that works for you. Even if you know you aren’t yet ready for a mortgage it is a good idea to:

At Richards Mortgage Group we believe in empowering our clients through information. We succeed when you succeed, and you succeed when you know what you are doing. To that end, we strive to ensure that communication, education, and accessibility remain the cornerstone of our brand. Like a guide with a compass and a map, we're here to help you understand where you are and how to get to where you want to be. Get in touch and we’ll be happy to help! Let's Cue Up a Discovery Call!

Quantus Mortgage Solutions

5053 11 St SE

Calgary, AB T2H1M7

Canada

T: 403.238.3111