More About Mortgages

for Canadian mortgage borrowers

There is lots to learn about mortgages, especially if this is your first, or your first in a long time. This page covers some of the more important terms you will come across on your mortgage quest, and some of the decisions you will need to make including considerations. There is also a link to a glossary for other terms, just in case. We will weave into the discussion opportunities to reduce the life-time cost of your mortgage. We'll describe what documents you will see and when. Where more in-depth information is available or warranted, we will link out to those for your quick review.

First things first, a mortgage is simply a loan for a property. The mortgage contract is for a certain length of time called the term. Five years is the most popular term for mortgages but there are other terms for as little as 6 months and up to 10 years. Prior to the end of your term, you will need to renew your mortgage contract for another term. A renewal is easy assuming you have paid on time as agreed with the lender and your credit rating is still good.

You keep renewing your mortgage until your house is paid for in full. Your mortgage payment is calculated by targeting how many years you would like to fully pay off your loan from start to finish if you made the same payment every month - this is called the amortization period. If you renew your mortgage term every 5 years, a mortgage set at a 25 year amortization would take the initial 5-year contract term plus 4 renewals to completely pay for / amortize your mortgage. The maximum amortization permitted for low down payment house mortgages is currently 25 years in most cases.

If you sell your house or move, you can usually take your mortgage contract with you (called a port) to the next house (upon re-qualification), or cancel it subject to a penalty.

The mortgage rate is the rate of interest you are expected to pay to the lender in compensation for the money that you borrow. Think of it as the rental rate for money. The mortgage rate offerings available to you will depend on a number of factors such as the contract term, the property-type, your financial situation, and external economic factors affecting all interest rates.

As we have discussed on other pages, the approval process is a journey from information gathering, asking the question "Can You Get a Mortgage?" and hearing a yes, a Pre-Approval where you provide and we review your income support documents, application, and credit, and finally the "live" Approval where all of your hard work pays off.

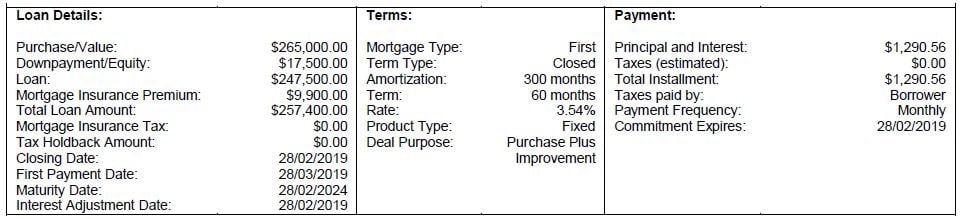

At the live approval stage, we formally make a request for a mortgage approval where we indicate the property that you want to finance, information about you, and the specific mortgage terms (characteristics) that you are seeking. Upon reviewing and approving this request, the target mortgage lender issues something called a mortgage "Commitment Letter," which contains the essential terms that you have asked for and will be agreeing to. For example, if you are asking for a 5-year contract with a 25 year amortization, the Commitment Letter will provide for a 60-month (5 year) term and a 300-month (25 year) amortization. We are going to go through many of the terms you will find in the Commitment Letter next, and please refer to the graphic.

As you work your way down the list, follow the links for further information and to get context for some of the decisions you will have to make, then return here and continue your reading.

WARNING: Read your mortgage agreement / commitment letter carefully and be sure to ask about anything that you do not understand. All federally regulated financial institutions must provide you with certain information about your mortgage in the loan agreement as described above. This information must appear clearly in an information box at the beginning of the mortgage agreement.

Having read the above, you are welcome to register your mortgage needs or things you would like to discuss further using this form Mortgage Feature Selection

To save money over the life of your mortgage, there are a number of steps that you can take, and decisions to be made about an appropriate mortgage lender.

Return to Can You Get a Mortgage' Overview

Borrowed Down Payment Mortgages

Other important mortgage features for first time buyers

Rent vs Buy Calculator

Free Guide: Paying Off Your Mortgage Faster

Free Guide; Three Steps to Successful Mortgage Shopping

7-Step Mortgage Approval Process Canada

I thought I was already pre approved for a mortgage!

Let's Get Started - I Need a Mortgage!

Quantus Mortgage Solutions

5053 11 St SE

Calgary, AB T2H1M7

Canada

T: 403.238.3111