How to Buy a House in Canada

Last Updated: May 2019

In the past few weeks, I have had a number of first time home buyer clients purchasing a home, some with the aid of a Realtor and others without on a For Sale By Owner (FSBO). With the aid of a real estate professional, a lot of the following questions get answered, but not always. When you are pursuing a FSBO, it's a lot tougher to figure the steps out, especially for the rookies.

![How to Buy a House [Read Guide]](https://no-cache.hubspot.com/cta/default/115190/430ef4af-ee71-4ea9-8c5c-2fede32e4fcd.png)

Here's an overview on the house buying process and steps in Canada.

- Mortgage Pre-Approval

- House Shopping and Price Discovery

- Offer to Purchase, Deposit and Home Inspection

- Mortgage Approval Process

- Closing, Get the Keys!

1. Mortgage Pre-Approval

A mortgage pre-approval is a very important step before you start shopping for a house. In fact, most Realtors will insist you have this as proof you are a qualified buyer and to make sure they only show homes in your price range. In this step, a mortgage professional will look at your finances and figure out the mortgage you can afford and provide you with mortgage advice.

![Can You Get a Mortgage? [Read Now]](https://no-cache.hubspot.com/cta/default/115190/8d35a884-2a8a-444b-9ae9-a8d85af5b10a.png)

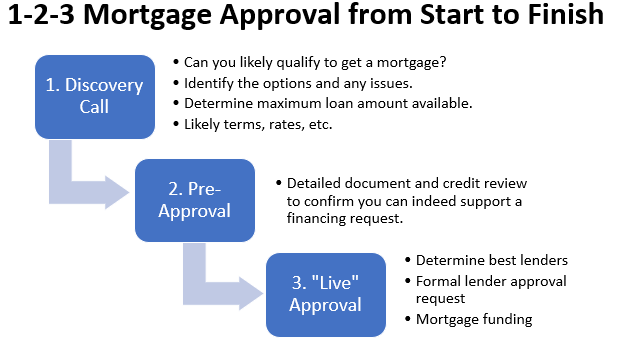

There are multiple stages of mortgage approval. It is important to recognize the difference.

- The first level of assessment, which I call a pre-assessment, is simply a 10 minute discussion about your finances, employment and credit to give you an idea about what you can afford. • typically you are not asked to provide any sort of paperwork. • please do not rely only on this pre-assessment discussion to shop for houses - ask for a more rigorous pre-approval if you want to start shopping.

- The second level of assessment is the more rigorous pre-approval, which means you provide your mortgage professional with a detailed credit application and authorization to review your credit file. • you will be asked to provide paperwork to support your application, such as proof of employment/income, down payment/equity, etc. • ask for a Pre-Approval Certificate, which shows your Realtor there should be no surprises when the time comes for your actual approval. • a pre-approval does not bind you to any particular lender and you can also request a "rate-hold" to protect yourself from rising interest rates.

If you are interested in either of the above pre-approval services, feel free to contact us. There is no charge.

Please keep in mind that a pre-approval is NOT a guarantee that your final mortgage request will be approved. Sometime your circumstances might change after the pre-approval, or lenders might not like the property that you want to buy.

The final stage, once you have finished house shopping is the "Live" approval in step 4 below.

2. House Shopping & Price Discovery

- Now the fun part, house shopping! Whether you are looking online, working with a Realtor, or see a "for sale" sign on a front lawn, you narrow your search down to homes that appeal to you and that are in your pre-approved price range.

- Remember, you don't always have to buy the maximum house you can afford. Have you heard the term "house poor"? It means your payments are so high you can't afford to have fun anymore.

- If you are working with a Realtor, they will arrange a viewing, where you can go through the house to see if it is a fit. Or for a FSBO, the seller will show you around.

- If you like the home enough and it meets your criteria, maybe you want to make an offer to purchase .. but at what price?

So let's talk about the term "Price Discovery"

- Just because the seller is asking $350K and their neighbor is asking $350K for a similar house, that doesn't mean the market price is $350K. They could both be off their rockers! They could ASK for $500K - doesn't mean they are going to GET it.

- So "price discovery" is the steps you go through to determine the most you are willing to pay for a home. This involves research on your part, and the more the better.

- If you are working with a Realtor, they can help with the research by providing some information on "comparable" homes that recently sold in the neighborhood and what they sold for.

- Here's a TIP: in ADDITION to asking your Realtor to set you up to automatically receive an email alert each time there is a new listing in your target area, style, and price range, ALSO request auto-emails triggered whenever a property sells including the sales price and days on the market (DOM). Ask for historical sales reports as well and do your homework.

- With good price discovery habits done in advance, when a property comes up, you should have a pretty good idea whether to make an offer to purchase or not. Good deals go fast, so be prepared!

3. Offer to Purchase, Deposit and Home Inspection

- If you want to make an Offer to Purchase, you have to deliver the correct form to the seller. Your Realtor should do this step for you, or if you are not working with a Realtor, then you want a lawyer or mentor to help you get the form done correctly. For example, our office often provides a "second set of eyes" on FSBO deals for our clients.

- The offer contains names of buyers and sellers, the price, things included and not included, amount of your initial deposit (usually 1-2% of the purchase price), the possession or closing day, and "conditions of purchase," such as you must get approved for mortgage financing and property passes inspection by a certain date called the condition dates. You give the seller about 24 hours to accept your offer or it expires.

- When the seller is presented with a written offer, they can either Accept it, Reject it, or Counteroffer. Any time someone makes a change to a contract, the change has to be initialed by ALL parties to be valid, otherwise the entire contract is dead with no obligation by either party to revive the deal.

- If the offer is finally agreed to and accepted, the contract will specify that the Buyer has to make the initial deposit within a day or two via cheque "IN TRUST" to either the Realtor's or a lawyer's TRUST ACCOUNT, but never ever ever to the seller.

- The deposit money has to sit in the trust account and no one can touch it until you get the keys, or if the deal falls apart (conditions of purchase not met), then you get the money back. Be prepared to make the cheque as soon as your offer is accepted.

Don't Pop the Champagne Corks - Home Inspection Time

- There is an old saying, "don't fall in love with the wedding, fall in love with the groom/bride"

As it relates to your "dream home", what might appear great on the surface, could be a moldy mess behind the walls, or expensive problems in the pipes, drains, and wiring. The neighbors might have an aggressive barking dog conveniently gone while you were viewing. Do your homework! Don't buy some one else's problems!

As it relates to your "dream home", what might appear great on the surface, could be a moldy mess behind the walls, or expensive problems in the pipes, drains, and wiring. The neighbors might have an aggressive barking dog conveniently gone while you were viewing. Do your homework! Don't buy some one else's problems!- A home inspector is a professional that goes through the property looking for problems. While they will not provide a guarantee against future problems, they are trained to at least give you warning about potential issues. Ask for a referral or look online. Cost is usually $400-$600.

- Book your home inspection to occur about a week after your offer is accepted to give the mortgage approval process a head start.

4. Mortgage Approval Process

Now is the time to actually get a mortgage. The mortgage approval process is similar to the mortgage pre-approval process, only now there is a specific property added to the mix. The mortgage lender must also approve the property.

- First step ASAP is to make sure you send your mortgage person a copy of the Purchase Agreement, complete and signed / initialed correctly, and the property information sheet like the MLS-feature sheet. Then you wait!

- On receipt of the Purchase Agreement and MLS-info-sheet, your mortgage professional (we) will review your application and all the other papers in your file, update your application, then "submit for mortgage approval" to the best mortgage lender/product for you.

- During normal times, we hear back from the lender within 24-48 hours, so day 2 or 3 after we receive your purchase agreement. Assuming the lender is interested in providing you a mortgage, they will provide a conditional approval (a "mortgage commitment") along with a list of documents they want to see from you to support your application. That's why it is important that your mortgage support documents are already in a file with your mortgage person, in advance of making an offer (ideally during the pre-approval process).

- Once we have a conditional mortgage approval, we review the terms with you, and you accept the lender's mortgage offer if satisfactory by signing it.

- In addition to support documents already in your file, we may ask you for some updates, like most recent pay stubs or bank statements for example, and forward all to the lender.

- The lender's "underwriter" reviews all your mortgage support documents, and checks them off their list if satisfactory. If they have questions or require further documents, you and we must respond ASAP.

- When the mortgage loan conditions are all met, the lender gives us a "file complete" (final approval) and then sends "mortgage instructions" to your lawyer's office. Think of the mortgage instructions as the lawyer's to-do list.

At this point, you or your Realtor are able to advise the seller in writing that the mortgage approval condition (and any other conditions) of your purchase are satisfied. You now have a FIRM deal - pop the champagne!

At this point, you or your Realtor are able to advise the seller in writing that the mortgage approval condition (and any other conditions) of your purchase are satisfied. You now have a FIRM deal - pop the champagne! - Between now and closing, you need to hire your movers, line up fire insurance for the new property, arrange for utility connections, make address changes, etc. Have fun!

5. Closing - Get the Keys!

- Closing Day is the day when you get legal possession of the property and the keys. The house becomes your home!

- A week or two prior to closing, you will need to meet with your lawyer to sign the necessary final papers, including the actual mortgage contract, and provide the balance of your down payment funds.

- On the closing day, your lawyer will combine your down payment with your initial deposit, request the mortgage funds from your lender, then pay the seller in exchange for the keys and land title to the property.

- Normally, you can get the keys around noon or early afternoon.

So that's a brief overview of the house buying process. First step should always be a mortgage pre-approval, then enjoy the ride. Contact us if you have any questions, or you're ready to get started!

Visit our new Comprehensive Home-Buyer's Guide for a more in depth overview of the process

.jpg)