Before you can buy a house, you need to make sure you can afford it and that there will be financing options available to you. This is where a pre-approval comes in. As mortgage lending criteria has become more strict over the years, the pre-approval and the increased certainty and confidence that goes with it has become an essential first step for the would-be-home-buyer.

What is a Pre-Approval?

A pre-approval is one of the very first steps in the home buying process and is intended to verify whether a potential buyer can qualify for a mortgage and how much they can afford to pay for a property between the mortgage they can qualify for and the down payment they can provide.

A pre-approval is not a guarantee that mortgage financing is approved, since there are still property specific criteria that must be considered once you have found a desired property, but when done properly it should provide a strong indication of how much mortgage you can qualify for and any potential obstacles that may stand in your way. This should give you the confidence and knowledge to shop the market and negotiate offers.

A pre-approval is not a guarantee that mortgage financing is approved, since there are still property specific criteria that must be considered once you have found a desired property, but when done properly it should provide a strong indication of how much mortgage you can qualify for and any potential obstacles that may stand in your way. This should give you the confidence and knowledge to shop the market and negotiate offers.

How Do I Get Pre-Approved for a Mortgage?

The first step to getting pre-approved is to choose a trustworthy mortgage professional to work with and get in touch. It's important to note that there is no official standard for a pre-approval, and sometimes the word get's used rather loosely, so make sure you work with someone who knows what they are doing. Our pre-approval process looks something like this:

- You decide you want to get pre-approved to buy a house and reach out to us by phone or by filling out a form on our website.

- After an initial discussion, if it sounds like a pre-approval would make sense based off of the information you provide, we will send you a "Let's Get Started" pre-approval package containing an application form, privacy consent form, and a list of documents that you will need to compile and submit to us for review.

- Once we have the application and privacy consent forms signed and returned to us, we are able to pull your credit report and confirm that your credit history meets the requirements to get a mortgage.

- As the rest of the requested documents come in, we review them in context with your credit report and property objective as indicated in your application form. The goal is to determine whether you have sufficient income, credit, and down payment to support the additional mortgage debt for your stated property objective.

- If everything checks out after a thorough document review, we then inform you that you are pre-approved for a certain amount of mortgage lending under certain conditions and that you are free to go shopping with your realtor for a property that conforms with the criteria of your pre-approval.

- Once you have found a property and negotiated an accepted offer, we then move on to the "live" approval stage of our mortgage approval process where we submit your application and property details to an actual lender and request funding.

![Can You Get a Mortgage? [Read Now]](https://no-cache.hubspot.com/cta/default/115190/8d35a884-2a8a-444b-9ae9-a8d85af5b10a.png)

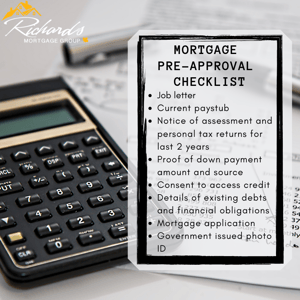

What Documents Are Required for a Pre-Approval?

The documents required for a pre-approval are situation specific, but generally can be broken down into 5 categories.

- Personal Information - This category includes identity documents, your SIN number, the filled out application, and situation specific documents such as citizenship/immigration documents and separation/divorce agreements.

- Income Documents - Depending on how you earn your income, this category will request a combination of documents that will be used to prove to a lender that you consistently earn enough to afford additional debt. Income documents can include pay stubs, tax documents such as NOAs and T4s (all taxes must be paid), letters of employment, disability documents, pension documents, child support and alimony documents, business financial statements (self-employed), and corporate tax fillings (self-employed).

- Credit Documents - The main document pertaining to your credit is your credit report. The credit report that mortgage brokers use is different than the reports that are available to consumers online and contains more information. Before we can pull your credit report we need your written permission on our privacy consent form. Other documents relating to credit include bankruptcy and consumer proposal documents and payout statements for various debts.

- Down Payment Documents - These documents include bank statements, transaction histories, copies of deposit checks, signed gift letters, investment account statements and documents proving the sale of certain assets. The goal of down payment documentation is to verify that you have enough money readily available to supply your agreed upon portion of the asking price, and that it was legitimately obtained.

- Property Documents - Although a pre-approval typically happens before you have a specific property in mind to purchase, if you already own any other real estate, you may need to provide mortgage statements, property tax statements, title documents, and proof of condo fees. Once you have found a property that you wish to buy, we will need an mls or other feature sheet with information such as the legal description, property tax amounts, condo fee amounts, and important property characteristics such as location, foundation, size, garage, heat source, water potability, and septic system.

What Are the Benefits of a Pre-Approval?

The main advantages of getting pre-approved before shopping for a home are clarity, confidence, and the ability to act quickly. You'll have clarity as to what you can afford, where in the market you should be shopping, and what your next steps are. You should feel confident that you have done your due diligence and that there are no unexpected surprises to derail you. And as a result, you will be able to act quickly and negotiate effectively when you find a property that meets your requirements.

Additionally, a thorough pre-approval constitutes much of the initial documentation groundwork for a full approval and will speed up the approval process. This is helpful when financing deadlines may be tight.

Finally, with a pre-approval in hand you will have much better luck being taken seriously by realtors, sellers, and other real estate professionals.

What Are Some Common Pitfalls to Avoid?

One of the most common mistakes that inexperienced buyers make with regards to a pre-approval is to assume that all pre-approvals are the same. Since there is no official definition of a pre-approval, the word sometimes gets used to describe less rigorous processes than the one described above. Some mortgage professionals and bank specialists might do as little as get you to fill out an application and run some initial calculations before telling you that you are pre-approved. While these less robust processes may be quick, simple and easy, it's important to remember that they don't guarantee anything and are less reliable than a thorough documentation review.

Another common mistake is to assume that a pre-approval is the same thing as a commitment and that because you have been pre-approved, you don't need to include a condition of financing in your offer to purchase. This assumption is false and can get you into a lot of trouble if you unconditionally commit yourself to purchase a property only to discover that the property itself doesn't qualify to be mortgaged even though you were personally pre-approved.

When combined, the two false assumptions above can be downright disastrous. Our goal is to help empower and educate you as a home-buyer so that you can make informed decisions and avoid assumptions. If you would like to work with us and are ready to get started with a pre-approval, please click the button bellow or reach out through one of the many other contact points on our website.