About 1 in 6 working Canadians are self-employed and, in recent years, the self-employed mortgage qualifying rule book has changed considerably. These evolving rules have created significant challenges for those seeking mortgage financing, and the property you can qualify for might not be what you expected....

It really comes down to INCOME - how much you make, whether you can prove it , and the filing and payment status of your personal income taxes with the Canada Revenue Agency or CRA. When you apply for a mortgage, you must prove – in some fashion – that you make enough money to safely pay your mortgage and other debts, and there are three methods (below). The income confirmation methods available to you will then dictate your minimum required down payment, extra costs you might have to pay, and the interest rates available to you at mortgage time.

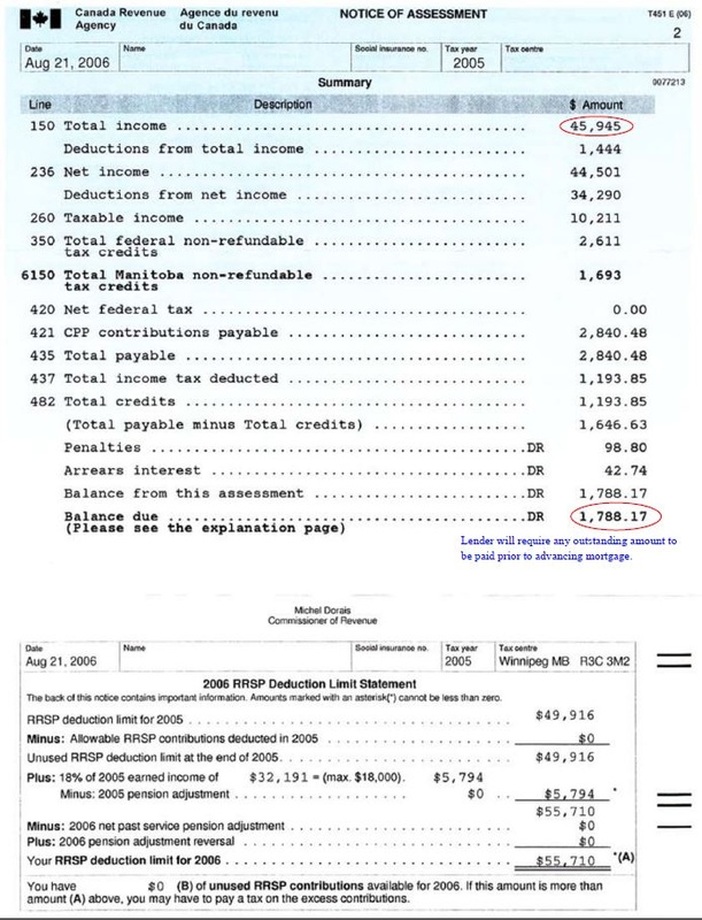

- Traditional Income Confirmation (the norm for employees) means that 1) you do make money, 2) your income is sufficient to support the mortgage payment and your other debts, and 3) you consistently report the income every year on your personal tax return, which then shows up on your Notice of Assessment line 150 as Total Income. If so, you can get a mortgage with as little as 5% down payment and at best interest rates. If you don't declare much income, then things get harder...

- Non-Traditional Income Confirmation means that 1) you do make money, 2) you can prove you make enough money with a combination of banking statements, business financial statements, business tax returns, etc., but 3) the income does not show up on line 150 of your personal tax returns. If this is you, your minimum down payment is now 10%, your CMHC-insurance risk premium just went up a further 2.75% of the loan amount, your interest rate is a touch higher, and the types of property you can own are restricted (yikes)!

- Stated Income means you are unable to confirm your income and federally-regulated banks must tag your mortgage as "non-conforming." If this is you, your down payment will need to be at least 20% (and as much as 35%), interest rates are at least 1.5x higher, and further restrictions on the type and location of the property you can finance are added to the mix. Private or alternate lending sources have stepped up to fill the gap, as many of the banks have now bowed out of this category.

In summary, how you report and declare your self-employed (or tip/ gratuity) income needs careful consideration and the advice to minimize your reported income at tax time could BITE YOU HARD at mortgage time, leading to either a "rejected" outcome, or added expense, headaches and restrictions. The good news is that a competent mortgage advisor in conjunction with your accountant can help you “manage your Line 150”, and there are options. You should know this information well in advance. Please feel free to contact us to discuss your specific situation.

.jpg)

{kind=link}