Many newer mortgage borrowers in Canada have never seen mortgage interest rates with any rate starting at 4% or higher. For others, you might recall when mortgage interest rates hit a staggering 21% in the early 1980s. This article is directed to anyone who has a mortgage renewal coming up in the next 18 months and is worried about how much higher their replacement mortgage payments will be, plus strategies to reduce the payment and to manage the stress.

Quick Mortgage Payment Increase Calculation

Let me start by providing you with a quick estimate of your upcoming mortgage payment when it comes time for renewal. Based on my assumptions that your mortgage had a 25-year amortization period and your renewal rate will be 2% higher than your previous mortgage rate from 5 years ago, you can expect an approximate 20% increase in your next mortgage payment. This relationship holds true for a 1% increase in rate as well, resulting in a roughly 10% higher payment. In other words, the payment increase is about 10 times the rate increase, establishing a clear correlation that can help you anticipate your payment increase at different rate differences.

| Example mortgage rates | With a rate increase of | Your payment will increase ~ | |

| Before | After | ||

| 3.54% | 4.54% | 1.00% | 10% |

| 2.69% | 4.69% | 2.00% | 20% |

| 1.89% | 5.09% | 3.20% | 32% |

Example: if your current mortgage payment is $2000/mo, and your renewal rate is going to increase 1.8%, expect an 18% increase to your new mortgage payment making it $2360/mo (1.18x10x$2000) for your renewal. If you would like help with the math under different assumptions, please click here to request a custom rate increase assessment.

Should You Shop Around / Switch to a Different Lender at Mortgage Renewal Time?

That's a great question. It depends. If your current mortgage lender is offering a competitive renewal rate and you can manage the new higher payment, accepting their renewal offer may be the path of least resistance, as you do not have to requalify.

However, if your current lender is not competitive (happens all the time) OR they cannot help you to manage your pending payment shock, then yes it's a good idea to shop around. Please keep in mind that all of your options to shop around at renewal time and hence to manage your payment shock hinge on your ability to mortgage-qualify when the time comes with the next lender, which would be required. That means acceptable and enough income to cover your new mortgage payment, property taxes, and your other consumer loan payments (car for example). If you have had a change in employment income (self-employed, one income vs two, non-guaranteed hours, etc.) or new consumer debts, then re-qualifying with a different lender might not be possible, so you may want to get a pre-renewal mortgage-qualifying check-up.

Let's Assume You Can Re-qualify for a Mortgage at Renewal Time

Assuming you can likely mortgage qualify with a different lender and want to keep your new payment in line with the current payment, let's dig in to some options.

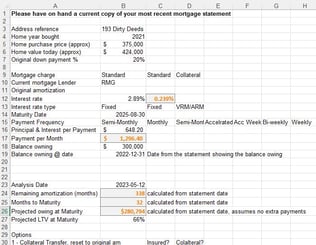

Option 1 - Collateral Transfer: When you last got your mortgage, depending on your lender, they may have registered what is called a Collateral Charge mortgage (vs. a Standard Charge). Tip - lenders that often register collateral charge mortgages include TD, ATB, Scotia, Manulife, CIBC, BMO, RBC, National Bank, B2B, to name a few (especially true if you have a home equity line of credit).

If you do have a collateral charge mortgage and desire to "switch/transfer" (what we call it) to a different lender, a number of lenders theses days are able to re-extend amortization back up to 25 years on insured and insurable collateral transfers. As examples:

- Resetting your amortization 5 years (from 20 back to 25) will result in only a 5% increase in your mortgage payment

- Resetting your amortization by 10 years (from 15 back to 25) will result in a 15% decrease in your mortgage payment.

So the above clearly illustrates the potential to manage your payment amount to suit your financial situation if you currently have a collateral charge mortgage.

Option 2 - Standard Transfer: Even if you have a Standard Charge mortgage (which is common with non-bank lenders such as Merix/Lendwise, MCAP, First National, RMG, CMLS, RFA/Street, etc.) *and* you have made accelerated weekly or bi-weekly payments, or made extra payments besides your regular payments during the course of your mortgage, or you have extra money now to put against the mortgage, you can reset the amortization to the original amortization (say 25 years) less elapsed time (say 5 years), which serves to increase the amortization back to 20 in this example. With the new mortgage, make your new payment only once per month or select non-accelerated weekly or bi-weekly to make the payment as low as it can go. As an example:

- if you made accelerated bi-weekly payments for 5 years on a 25 year AM mortgage, your remaining amortization will be about 17.2 years. This remaining amortization can be increased back to 20 years (25-5) at renewal time, which would limit your payment increase to about 7% based on a 2% point rate increase (a ~3.5x relationship between rate increase and payment increase, down from 10X).

Option 3 - Refinance: In options 1&2, we mentioned "insured or insurable" mortgages, which means the mortgage was CMHC-insured or meets the requirements for CMHC/Sagen/CG mortgage default insurance (under $1M in home value and a loan amortization not to exceed 25 years), and qualifies for lower rates. Otherwise the home loan is considered non-insurable, and you must have at least 20% equity in the property at the time of refinance.

While refinance mortgages have slightly higher interest rates, the good news is that you can re-extend your amortization out to as much as 30 years and you may also be able to consolidate some other consumer debts into the home loan thereby improving your overall cash flow. You may even find that your new mortgage payment falls below its current level. If you are really concerned about affordability and you likely have 20% home equity, this option might be just what you need to keep things under control.

In conclusion

- First and foremost, if you want to preserve your option to switch lenders at renewal time, click here to get a situation review today. We are happy to help you determine if you'd likely have any re-qualifying issues and answer any of your what-if questions. This knowledge may give you the time you require to plan and make appropriate financial and spending decisions.

- If you'd like us to help you renew your mortgage with a great rate and manage your next payment using one of the strategies/options above, we're happy to help also. A copy of your most recent (year-end) mortgage statement will give us the data we need in our analysis.

We'll present your options to you once our analysis is complete. You can kick-start the process with a mortgage renewal situation review request <click here.

We'll present your options to you once our analysis is complete. You can kick-start the process with a mortgage renewal situation review request <click here. - Finally, as with most things in life, you can minimize the negative impacts of many things by taking action early and checking your assumptions. An ounce of prevention is worth a pound of cure, as the saying goes. Even if you just want us to contact you 120 days from your next renewal date so we can give you a renewal quote and options at that point in time, you can register your mortgage renewal date here.

.jpg)