Hey - if you are reading this, tell everyone you know that if they ever want to buy a house, you have to work on your credit score well in advance.

Advance Preparation for a House Purchase - Your Credit Score

As a mortgage broker, I constantly see young people trying to get into a mortgage to buy their first home only to discover they don't have any credit history established or the credit history they do have is insufficient or tarnished. It takes time and effort to create or fix your credit score. That's the point of this article: It Takes Time, so Get to It! :)It is assumed that most of us cannot afford to pay cash for a home, so a mortgage become necessary to raise the appropriate amount of funds for a purchase. Credit Score is a major determining factor in lenders deciding whether you get the best mortgage rate or a REJECTED on your mortgage application. If you are preparing to buy a new home, here are a few tips to make sure your credit score supports your home buying plans.

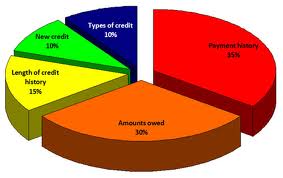

1. A person needs active trade lines to get a credit score. Trade lines can be credit cards, lines of credit, loans, car leases etc. Rent and paying bills does not show up on your credit bureau (unless you don't pay!) so they don't create or increase your score!

Here's the simple truth: You must borrow and repay to create a history of your debt repayment habits! Use the credit you have regularly to establish and/or maintain a credit history. For example, use your credit card for gas, groceries, or one small purchase every month and pay it off every month <-that's good! Having zero credit use diminishes trustworthiness in eyes of the credit bureau <-that's bad!

2. Obtain at least 2 trade lines (credit cards, loan, etc) with at least $2500 maximum limit between them. Under $2500, the lender may not take the credit card activity seriously. Consider credit cards at a store you don’t shop at, or a gas card if you are worried about over spending.

3. Pay bills on time as agreed. Late, missed and unpaid bills lower your score. Set up automatic payment and overdraft protection on your bank account. (Paying one day late is NOT paying as agreed!)

4. Think twice about allowing someone to credit check you...multiple checks lowers your score...makes you look like you NEED money. Not to mention, not all credit checks are equal – “B” lenders (say a pay-day-loan) may drop your score more than “A” lenders!

5. Never max credit cards etc...stay below 30% of card limit for the best score and below 50% for next best score. High balances lower your score. Going over your limit is a score killer!

6. Finally, treat your credit like an asset which can maximize your buying power.

For more information, check out the credit bureau links TransUnion and Equifax.