Getting approved for a mortgage can be very stressful on first time home buyers... this article explains what is really happening!

Getting approved for a mortgage can be very stressful on first time home buyers... this article explains what is really happening!

Last Updated; June 2022

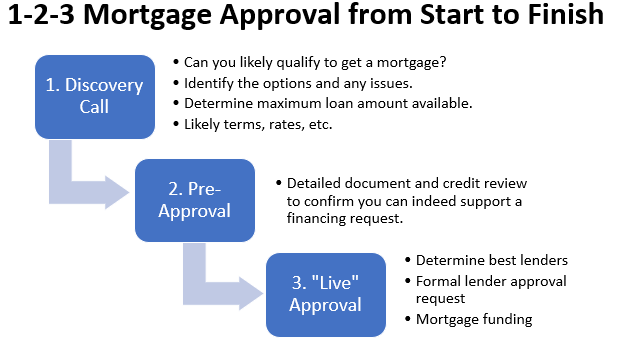

When a person thinks they are "pre-approved" for a mortgage by a mortgage professional, it can mean different things depending on who you (the borrower) are dealing with and the robustness of their "pre-approval" process. As a minimum, it could mean "based on what you have disclosed about your income, debts, down payment, credit, and the property, etc. at a particular point in time, you should qualify for a mortgage to $X." The italics above put a lot of onus on you to accurately interpret and disclose your financial situation in a manner identical to how the mortgage qualifying rules would actually be applied. If you never provided an up-front mortgage application and supporting documents as part of your "pre-approval" process, alarm bells should be ringing.

Here is where things come of the rails - you make an offer to purchase, but no one has actually received or reviewed your *full* support documents to confirm they *all* meet the qualifying rules. Now you are scrambling and perhaps in for a nasty surprise.

Even if you have provided some upfront documents to your mortgage professional, it is important to note that the mortgage pro/rep is NOT the lender's underwriter/decision maker. An actual underwriter seldom reviews your information in any detail until there is a real deal and only then because it takes a lot of time and resources. Things can also change in your finances and the market after your pre-approval, so the loan underwriting is deferred until there is an actual "live" deal. This this puts the onus back onto you as the borrower to make sure the pre-approval process is robust.

When you have an accepted "live" offer on a property, it is then that we (you and your mortgage pro) have to prove everything you have said is still true plus provide details about the exact property the lender will be putting a mortgage on. In the purchase contract, there should be a financing condition date, meaning you have a certain amount of time (week or two) to arrange financing and prove what you said in your application is true. (It's a document intensive process, and if you are just starting to collect documents now, you are going to find it a lot harder than getting a car loan!)

As a first time home buyer, my advice is to work with a good mortgage broker well before making an offer to purchase. They should anticipate and task you to provide the documents the lender will want to see, review them, and give you a professional opinion as to the likelihood of an approval when the time comes. Often they can make helpful suggestions on how to improve your odds. Getting your ducks (and documents) in a row allows the broker to present your application in the best light possible and be ready with all your documents when the lender asks to see them, vs. a mad scramble for documents after you have an accepted offer.

When you go "live," a lender's "underwriter" will review your electronic application. If they like what they see and CMHC agrees to mortgage default insurance, they will issue a formal "mortgage commitment," with conditions. The conditions will be .. prove your job, income, closing costs, property purchase contract, property details, appraisal value, etc....

At that point, as a mortgage broker, I would then provide the lender with your support documentation (which I like to collect and review in advance to prevent surprises!). It is only when the lender actually reviews all your documents and is satisfied with your proof that the "tick-boxes get ticked" and you are approved for a mortgage!

In the case of a PRIVATE deal (no Realtor involved), historically, there are much higher incidents of fraud so lenders are much more careful and extra work (including a physical appraisal) is often required.

Keep in mind that lenders, brokers, and appraisers are very busy at certain times of year (especially spring) So make sure your Realtor gives you, your broker and lender enough time when choosing a financing condition date to complete the process.

In summary, getting an actual mortgage approval involves a defined process that is the same for everyone and you and your broker/lender will work through the process step-by-step. Mortgage brokers will have many lenders and many solutions to choose from in most cases. This is why many buyers choose to work with an experienced mortgage broker over their bank - get to YES and APPROVED faster!

Do you want to reduce stress and pull-off your first mortgage and home buying experience like a pro? :) Happy to help!

.jpg)